Hard as it is to believe, it's already time for another ECB meeting. A lot of water has clearly passed over the bridge since the last one, and while the DAX is largely unchanged since that October 2 "rien fait" result, the IBEX is some 5% lower and BTPs are off by a point. More pleasantly, EUR/USD is actually a couple of big figures lower, largely as a function of USD strength engendered by the BOJ. (That, signor, is how you weaken your currency!)

Given the ongoing doldrums of the Eurozone, the seemingly daily collapse in oil, and the rather tepid take-up of the first TLRTO, there's a school of thought that Draghi and co. will loosen some of the requirements to participate. That, combined with the successful announcement of the bank stress test results, would putatively increase the incentive for banks to apply for loads more liquidity.

Or will it?

Unlike during the time of the original 3 year LTROs, there aren't exactly a lot of high-carry trades on offer, particularly at the short end of the periphery. While the spread between the refi and the deposit rate represents the actual cost of holding excess cash, and remains as low as it has ever been, one would have to presume that the act of "cutting a check" to the ECB for the privilege of parking cash there is one that many banks will wish to avoid.

More generally, of course, one can clearly question whether there's anything else the ECB can reasonably (and practically) do. Yes, theoretically they could engage in a swashbuckling BOJ-style orgy of monetary munificence....but there is no other central bank in the world where the chasm between theory and practice is so wide.

Moreover, while there is clearly a demand-related deflationary impulse in Europe, the genesis is a fiscal one, and there is little empirical evidence that any amount of monetary pump-priming can replace the salutary effects of time in resolving the problem.

At the same time, the trend of disinflation/deflation is a global one, caused in many cases by global factors. A by-no-means-exhaustive list includes the following:

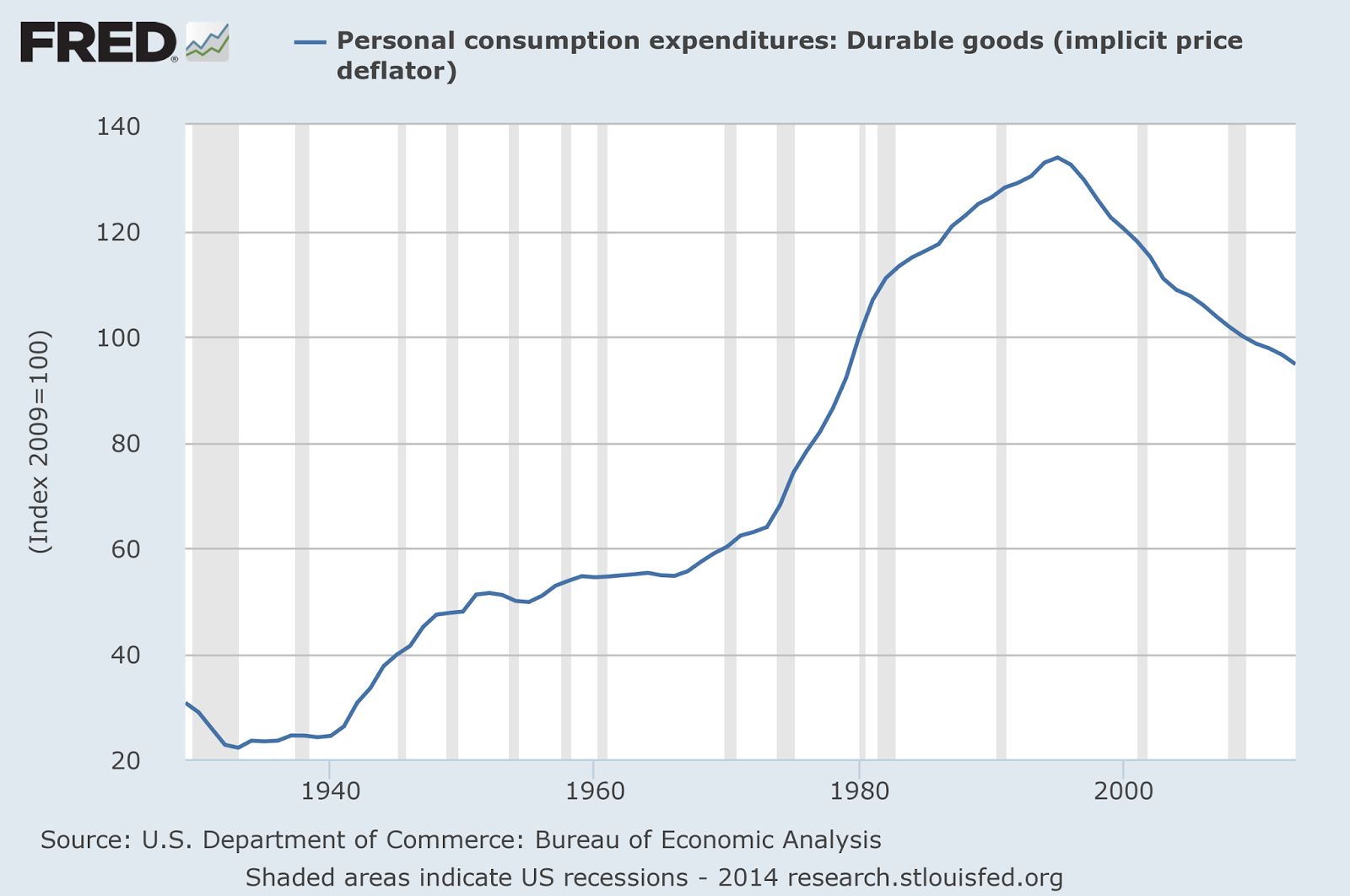

* Globalization has shifted the supply curve for many, many goods (and some services) much more abruptly than the demand curve; the equilibrium level of many prices has therefore shifted lower. Observe the PCE deflator for durable goods; although it also declined (by more, in percentage terms) during the Great Depression, the current 20-year secular decline reflects a structural supply shift rather than a shock-induced demand shift.

* Technology such as the Internet has had a profound impact upon the world economy in terms of efficiency of communications. Productivity in many aspects of economic life has shot higher as well (insert Facebook joke here.)

* The payoff of fixed investments is still being reaped or, in the case of the commodity sector, just starting to be reaped. Although the TMT infrastructure bubble didn't necessarily work out so well for many of the firms that did the work, it is a sunk cost the benefits of which are still being enjoyed today. Commodities, meanwhile, move in super-cycles given the extraordinary intensity of the capital expenditure required to bring new supply on-line. A glance of the last decade of the Australian dollar illustrates where we've been in that cycle; a brief trawl through some of the comments made by some of the usual-suspect resource firms should leave you under no illusions about where we're headed. At the same time, the world's largest fossil-fuel consumer has become less dependent upon global production.

None of these factors are particularly unique, but then again neither are periods of secular price declines or stagnation. Consider that the first transatlantic telegraph cable was laid in 1858. Eleven years later, the first transcontinental railroad across the United States was completed. These innovations, combined with the end of the Civil War, enabled the US to fulfill the 19th century role occupied by China today. US exports as a percentage of the global total exploded from 7.9% in 1870 to 13.2% in just 10 years. And what did inflation do during this period and its aftermath?

It was negative for much of the time.

Source: www.irrationalexuberance.com

Source: www.irrationalexuberance.com

So what does this mean for inflation targeting? A student of history might suggest that for central banks to target a completely arbitrary (positive) inflation figure against the tide of disinflationary/deflationary factors cited above (as well as others) is akin to King Cnut ordering back the waves or Xerxes the Great shackling the sea for breaking his pontoon bridge across the Hellespont.

In other words, futile.

In fact, worse than futile if their efforts to combat forces that are clearly beyond them (does anyone think any easing Draghi might do will positively impact the price of oil?) lead to substantial price distortions in items and assets that are more easily influenced by central bank policies.

Indeed, one could argue that this is the narrative of the last 20 years of central banking in the United States.

Of course, the realpolitik is that in a world still awash in debt, deflation is a distinctly unsavoury outcome. Small wonder, therefore, that in a world where schoolchildren get "participation awards" rather than winners' medals, monetary authorities are trying their damnedest to keep the balls in the air as long as possible to shield as many people as possible from unpleasantness. For better or for worse, the exaggerated economic cycles of 140 years ago are simply unpalatable- even though those countries that "took their medicine" during the crisis seem to be faring rather better than many of their peers these days.

None of this means that you should buy or sell euros or Spooz today or tomorrow. Sometimes, however, it's worth taking a step back and considering where we are in the very big (dare we say macro?) picture. It's certainly more interesting than wondering if and how the ECB might adjust their latest string-pushing exercise....

Given the ongoing doldrums of the Eurozone, the seemingly daily collapse in oil, and the rather tepid take-up of the first TLRTO, there's a school of thought that Draghi and co. will loosen some of the requirements to participate. That, combined with the successful announcement of the bank stress test results, would putatively increase the incentive for banks to apply for loads more liquidity.

Or will it?

Unlike during the time of the original 3 year LTROs, there aren't exactly a lot of high-carry trades on offer, particularly at the short end of the periphery. While the spread between the refi and the deposit rate represents the actual cost of holding excess cash, and remains as low as it has ever been, one would have to presume that the act of "cutting a check" to the ECB for the privilege of parking cash there is one that many banks will wish to avoid.

More generally, of course, one can clearly question whether there's anything else the ECB can reasonably (and practically) do. Yes, theoretically they could engage in a swashbuckling BOJ-style orgy of monetary munificence....but there is no other central bank in the world where the chasm between theory and practice is so wide.

Moreover, while there is clearly a demand-related deflationary impulse in Europe, the genesis is a fiscal one, and there is little empirical evidence that any amount of monetary pump-priming can replace the salutary effects of time in resolving the problem.

At the same time, the trend of disinflation/deflation is a global one, caused in many cases by global factors. A by-no-means-exhaustive list includes the following:

* Globalization has shifted the supply curve for many, many goods (and some services) much more abruptly than the demand curve; the equilibrium level of many prices has therefore shifted lower. Observe the PCE deflator for durable goods; although it also declined (by more, in percentage terms) during the Great Depression, the current 20-year secular decline reflects a structural supply shift rather than a shock-induced demand shift.

* Technology such as the Internet has had a profound impact upon the world economy in terms of efficiency of communications. Productivity in many aspects of economic life has shot higher as well (insert Facebook joke here.)

* The payoff of fixed investments is still being reaped or, in the case of the commodity sector, just starting to be reaped. Although the TMT infrastructure bubble didn't necessarily work out so well for many of the firms that did the work, it is a sunk cost the benefits of which are still being enjoyed today. Commodities, meanwhile, move in super-cycles given the extraordinary intensity of the capital expenditure required to bring new supply on-line. A glance of the last decade of the Australian dollar illustrates where we've been in that cycle; a brief trawl through some of the comments made by some of the usual-suspect resource firms should leave you under no illusions about where we're headed. At the same time, the world's largest fossil-fuel consumer has become less dependent upon global production.

None of these factors are particularly unique, but then again neither are periods of secular price declines or stagnation. Consider that the first transatlantic telegraph cable was laid in 1858. Eleven years later, the first transcontinental railroad across the United States was completed. These innovations, combined with the end of the Civil War, enabled the US to fulfill the 19th century role occupied by China today. US exports as a percentage of the global total exploded from 7.9% in 1870 to 13.2% in just 10 years. And what did inflation do during this period and its aftermath?

It was negative for much of the time.

So what does this mean for inflation targeting? A student of history might suggest that for central banks to target a completely arbitrary (positive) inflation figure against the tide of disinflationary/deflationary factors cited above (as well as others) is akin to King Cnut ordering back the waves or Xerxes the Great shackling the sea for breaking his pontoon bridge across the Hellespont.

In other words, futile.

In fact, worse than futile if their efforts to combat forces that are clearly beyond them (does anyone think any easing Draghi might do will positively impact the price of oil?) lead to substantial price distortions in items and assets that are more easily influenced by central bank policies.

Indeed, one could argue that this is the narrative of the last 20 years of central banking in the United States.

Of course, the realpolitik is that in a world still awash in debt, deflation is a distinctly unsavoury outcome. Small wonder, therefore, that in a world where schoolchildren get "participation awards" rather than winners' medals, monetary authorities are trying their damnedest to keep the balls in the air as long as possible to shield as many people as possible from unpleasantness. For better or for worse, the exaggerated economic cycles of 140 years ago are simply unpalatable- even though those countries that "took their medicine" during the crisis seem to be faring rather better than many of their peers these days.

None of this means that you should buy or sell euros or Spooz today or tomorrow. Sometimes, however, it's worth taking a step back and considering where we are in the very big (dare we say macro?) picture. It's certainly more interesting than wondering if and how the ECB might adjust their latest string-pushing exercise....

42 comments

Click here for commentsas you can imagine, AEP having a field day at the Euro's expense.

Replyhttp://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/11211973/Mario-Draghis-efforts-to-save-EMU-have-hit-the-Berlin-Wall.html

might be right this time though, the situation is untenable for the debtor nations, and support for taking back sovereignty is rising...

C Says

ReplyExcellent post. Why I remain an avid reader.

Indeed what is the point of targeting inflation/wages when these are influenced by so many parameters (which they dont know to some extend or they cannot measure)..

ReplyCBs should focus on financial stability instead...

King Cnut, Xerxes, Draghi - that's a lot of name dropping

ReplyAmen MM, amen ...

ReplyPart of the problem with the Eurozone discourse is that a large swathe of otherwise serious and clever commentators are still very annoyed that they didn't get the Euro break-up call right in 2012, and are therefore constantly doubling up.

Just as the proverbial 1987 crash in Spoos, it might happen today, tomorrow or in five minutes, but it makes for a deeply warped debate. The Eurozone is a deeply flawed entity, but that does not mean that the economy will collapse every two years. Ageing populations, high debt levels etc yield exactly an economy bumping along the zero line.

The (real)politik of the Eurozone clearly holds the potential source for a very painful uprising but sitting around and waiting for this (calling it day in and day out) is boring and worthless. This is especially the case as we have seen the movie so many times before. Chaos always comes before solutions in the euro area, and I don't see why it would be different this time, but as Polemic says, using all kinds of long-term arguments to justify short-term investment and trades make for poor decision making. Maybe the vote in Catalonia will snap a chain in Spain, maybe it won't ... I mean we can go on and on here ;)

On a more personal level, it is just bad for the spirit to wed yourself to a black swan/perrenial doom discourse. Be realistic, observe the downside risks, know that Eurozone politics move in mysterious ways and take it from there!

On Mr. Draghi ... well, he is obviously feeling the hangover from the OMT here, which is why he is seen as being behind the curve even though he is about to kick off the most aggressive QE program ever in the eurozone. Believe me, this will have a larger impact than many think, but will it generate jobs in Spain etc (well, you already know the answer here!).

Claus

Amen MM, amen ...

ReplyPart of the problem with the Eurozone discourse is that a large swathe of otherwise serious and clever commentators are still very annoyed that they didn't get the Euro break-up call right in 2012, and are therefore constantly doubling up.

Just as the proverbial 1987 crash in Spoos, it might happen today, tomorrow or in five minutes, but it makes for a deeply warped debate. The Eurozone is a deeply flawed entity, but that does not mean that the economy will collapse every two years. Ageing populations, high debt levels etc yield exactly an economy bumping along the zero line.

The (real)politik of the Eurozone clearly holds the potential source for a very painful uprising but sitting around and waiting for this (calling it day in and day out) is boring and worthless. This is especially the case as we have seen the movie so many times before. Chaos always comes before solutions in the euro area, and I don't see why it would be different this time, but as Polemic says, using all kinds of long-term arguments to justify short-term investment and trades make for poor decision making. Maybe the vote in Catalonia will snap a chain in Spain, maybe it won't ... I mean we can go on and on here ;)

On a more personal level, it is just bad for the spirit to wed yourself to a black swan/perrenial doom discourse. Be realistic, observe the downside risks, know that Eurozone politics move in mysterious ways and take it from there!

On Mr. Draghi ... well, he is obviously feeling the hangover from the OMT here, which is why he is seen as being behind the curve even though he is about to kick off the most aggressive QE program ever in the eurozone. Believe me, this will have a larger impact than many think, but will it generate jobs in Spain etc (well, you already know the answer here!).

Claus

CF Poland yesterday doing what I believe to have been the correct thing when all these factors are taken into account - yet being roundly chastised by the market for being short sighted or behind the curve. When deflation is driven by food, fuel and clothing, why should one cut rates!

Replythose countries that "took their medicine" during the crisis seem to be faring rather better than many of their peers these days

Replyhmmm, I'm not following you here. Are you referring to the recent crisis? It seems to me that most of the EU periphery is still taking their medicine, whereas the UK for example is using monetary easing to inflate away the private debt (mainly household debt). It's hard to argue that the former are faring better.

Love the post otherwise, and completely agree about the larger secular disinflationary trends.

Was really thinking of the little guys- Iceland and Estonia- that saw financial failures and a gut wrenching double digit negative GDP swoon after 2008, but that saw rather a better rebound than most of the rest of Europe.

ReplyWell, in both these cases, they had their own currency that promptly devalued (especially ISK), thereby helping with household indebtedness in much the same fashion as in the UK. Meanwhile Jose and Nikos are still fighting against deflation with a debt in a hard currency (and are possibly without a job too).

Replyvisited Iceland summer 2007 - everyone there kept on talking about Napoleon and how they 'fishermen' were then taking on Danish banks

Replywith their kroner at peak it was the most expensive country in the world

vanity vanity

MM - ud mentioned in ur previous post the probability of a gap close on spoos - do you see the low from 2 days ago as having completed that requirement? Also wanted to clarify if you meant just the most recent gap or the multiple ones spawned in this V hypernova for the last 2 weeks (i.e.1900ish,1960ish etc).

ReplyGreat article today btw.

@washedup: Was really referring to a very tactical call about the last gap, which thus far has not really panned out as I do not see the gap as having been closed (looking at SPYs).

ReplyThat was a good read, MM.

ReplyA lot better than my P/L this morning. Apparently another round of Draghi jaw-boning about how big his bazooka might be if and when it is deployed was enough for punters to sell more Euros, and we have yet another new high in DX. As our model called for DX to peak at 86, there has been a certain amount of pain since that level was breached. C'est la vie.

Draghi-san, you got nuthin'...

ReplyDoes LB get a "participation medal", MM?

Reply(silence)

Ah. I see.

In March 2012 the ECB's balance sheet was 2.98 trillion EUR. It is currently 2.03 trillion EUR. Draghi had better hope for an enormous take up of TLTRO #2, because if it is small then he's going to have to squeeze a whole lot of bond buying past the Germans.

ReplyWestern Select Oil new 2014 low of $60.26

ReplyDXY now just 1.5% below its 5yr high back in early 2009 . Back then , oil was @ $65 per barrel

ReplyMM - i found it interesting that Draghi mentioned specifically that other CB balance sheets would be contracting while theirs would be expanding - obv he means the fed (I am searching for any other examples and can't come up with any). Can't recall the last time any Cbanker presented the expectation for a different major CB's monetary trajectory as if it was a 'done deal'. Thought this comment was more relevant to FX from here than anything else in the speech.

Reply@ washedup, yes, clearly he was trying to make a point to encourage more currency weakness IMHO.

ReplyHave been trying to find a neat summary of the conversation that took place between Draghi and the rest of the ECB governing council, that lead to the 5 mentions of the word 'unanimous' in the press conference. These two seem reasonable proxies:

Replyhttp://www.starwars.stopklatka.pl/sounds/failedme.wav

http://www.moviewavs.com/php/sounds/?id=gog&media=WAVS&type=Movies&movie=Snatch"e=thinice.txt&file=thinice.wav

Yen tracking: South Korea Vice Finance Minister - South Korea to manage KRW moves in line with JPY

ReplyScotiabank expects the inflationary effects of Abenomics/BOJ's asset purchases to fizzle off by 2016.

Reply@ BB: that reminds me of one of my all time favourite Youtube clips:

Replyhttp://www.youtube.com/watch?v=vskHXtPuvBk

When DXY first broke above 86 last month it appeared to get the attention of the fed who talked it down. Now its at 88 - realistically what are the fed options? There is a big spread between dot plots and eurodollars already - to me this implies a limited effectiveness to fed pushing out or flattening rate expectations. People look back at the 80's and say how strong dollar can be fine but a lot has changed since then.

ReplyI don't see how this does not show up as at least headwinds for earnings, and lower prices for CPI etc.

The global hot-potato game of exporting deflation seems to be getting stronger and stronger. Currency wars indeed.

If the fed wanted to affect DXY, is forecast revision enough if the market already does not buy their dots?

Mr. T, perhaps the FED will leave this alone for the time being and let some crappy US data point do their work for them? With DX now homing in on 88, it's likely there will be no shortage of lousy US data just around the corner. The question is, with a USDJPY target now at 120, will DX be 90 before it turns?

ReplyMight be too early for this to be real, but the Challenger job cuts report showed a big increase for October, notably in retail.

October Job Cuts

There are already some layoffs in the shale patch, and despite what the CEOs are saying on TV, they all look a bit scared (presumably of their debt to enterprise value ratio) to me. This dollar surge is not going to be a one way street for the US.

While we are at the NSFW YouTube clips:

ReplyScottish Star Wars

Fed can hardly call for Europe to 'do more' and then not expect eur.usd to fall when they move that way . Don t think Fed will targey strong dollar other than note its effects on growth and react when the growth symptoms occur. The dream would be Growth constraints from strong dollar would be countered by benefits of stimulated european growth feeding thru to global/US side. But there is no cakey eaty solution here.

ReplyMeanwhile, in the Ukraine. ..... looks like this disintegrates tomorrow. Just in time for winter.

Replylet some crappy US data point do their work for them

ReplyMaybe I'm missing some part of the transmission mechanism, but the way I've been seeing it work is "crappy data leads to expectations of lower rates for longer". If the market is already expecting lower rates for longer (via out year ED etc) than what the fed is saying, isn't that transmission mechanism broken? ie if EDZ6 is saying 1.9% and the dot plot is saying 2.75%, then we get weak data and fed dot plots just converge on ED rates it's not clear to me that it will have any effect on markets.

Surprisingly, the fed has not asked me for my input, but I think their transparency efforts are getting in the way. Without the dots, markets would expect that the markets and fed are probably in sync. If there is a visible, persistent delta then it just makes the case for the fed being 'behind the curve' etc too strong.

Unless they want to open the possibility of more QE, the stage is set for DXY to really run without any way to reign it in.

partly echoing LB and T here, but i think the Fed would be at first inclined to see this as 'good' dollar strength and let the data prove otherwise - goes with dame Janet's (newfound or not) sympathies for the average Joe who benefits from a strong dollar than equity owners who ultimately do not - when MNCs start mass layoffs in a few quarters and a couple of EM's go banana splat with clear spillover implications for the US it could be a different story - so, certainly easier to see the dollar argument than get any sense of direction on spoos.

ReplyAltho, as T eloquently pointed out, not clear if things could be a little too far gone, and a bit too priced in for QE4 to ever be on the table (as opposed to newfangled alternative medicine via the fiscal route)

Mr T. In the short term, yes. We are all very much conditioned to the argument that "weak data" means "later hikes", so "buy stocks". What I am talking about is when we start to see REALLY WEAK DATA (not yet, for a month or two?) that impact profit forecasts. The usual recency bias says, no, it can't happen, but just look at Q1 '14.

ReplyMy argument is that BOTH EDZ6 AND the dot plot may prove to be much too optimistic about US growth in Q1-3 '15. I am sure there were some experts calling for Japan to grow at 3% in the 90s, but a deflationary mind set is stubborn once it sets in. Just as Europe faces disinflation driven mainly by demographic factors, so does the US.

A strong dollar is a significant headwind to US industrial and technology exporters, just as a stronger yen was a headwind to Japan Inc. at the end of the QE episodes. Since the US worker and consumer hasn't participated in the Trickle Down QE miracle, they are unlikely to be able to bail out the economy this winter. US retailers were laying people off in October, just when you might be expecting them to be hiring. That's a big hint that the holiday season might not be rip-roaring.

Bucky's recent parabolic moonshot is going to curtail 2105 growth quite sharply, at about the same time as Mr Market notices that the liquidity taps have been shut off. We will probably see 5y5y breakevens begin to price in the slowdown before it shows up in other metrics. The latest attempt at US housing reflation is already dead in the water, despite extremely low mortgage rates. No demand. Not at these prices.

LB where you are getting the data about retailers laying off into the holidays? Everything I'm reading speaks to noticeable y/y increases among the big ones.

ReplyTibia's new piece is in rolling stones

Replyhttp://www.rollingstone.com/politics/news/the-9-billion-witness-20141106#ixzz3IJNagNqG

it's big

Challenger announced October layoffs data this morning, retail was the largest sector in that report. It was a bit of a surprise to me as well, although most stores in Plugtown are empty. We are aware that things are different in Hedgeville.

ReplyThe AA II Bull/Bear ratio has soared again and is now at highest levels this year, QE or no QE:

Sentiment Extremes

Mr Market has been known to sell such extremes in retail investor sentiment, irrespective of the result of NFP bingo.

Oh, twist my arm, I'll have a go. +215k, only a bit short of the consensus number of +240k. Go on, Claus, have a pop. You know you want to.

epilogue: US equities beat European equities dance to Draghi bazoukous

ReplyLB I think you might have misread that report - retail hired 144k and laid off 5k. Retail topped the "hiring announcements" not "layoffs".

ReplyMr T:

ReplyI was surprised myself. Here it is. We can't be looking at the same data:

Challenger Job Cuts

Just one month after falling to a 14-year low, monthly job cuts surged nearly 70 percent in October to the second highest total this year, according to the report Thursday from global outplacement consultancy Challenger, Gray & Christmas, Inc.

U.S.-based employers announced 51,183 job cuts last month, a 68-percent increase from September’s 30,477, which was the lowest monthly total since June, 2000 (17,241). October job cuts were 12 percent higher than the 45,730 layoffs announced during the same month a year ago.

The October total is not only the second highest of the year behind May’s 52,961, but it marks only the fourth time in the last 22 months that job cuts exceeded 50,000.

“While it is too early to say for certain, the October figure may mark the kick-off to a fourth-quarter surge in job cuts. It is not unusual to see the pace of downsizing accelerate in the final months of the year, as employers take measures to meet year-end earnings and profit goals,” said John A. Challenger, chief executive officer of Challenger, Gray & Christmas.

October job cuts were led by the retail industry, which announced 6,874 planned layoffs during the month. That is nearly 3.5 times more than the 1,965 job cuts announced by retailers in September. To date, these employers have now announced 38,948 in 2014, second only to the computer industry.

Guess what chaps...there are both job cuts and hiring announcements...that's what's known as labor market turnover or 'churn.'

ReplyYou have to look at the net of the two to get net job creation figs, obviously. From what I can see, the numbers looks pretty good...Challenger has net job creation of ~96k in October 2014 vs ~42k a year ago. Holiday hiring plans are up 35% y/y.

http://www.challengergray.com/press/press-releases

Yeah, yeah. But what about the Advance-Decline line?

Replyafter i dropped contemporary art auction records i have now dropped my favorite Sotheby's share price 'too much fucking ridiculously concentrated money in this world'indicator and will now exclusively use:

Replythe new 'divorce settlement bubble' indicator

currently standing at FOUR point eight billions for Elena Rybolovleva

who is still not quite happy and battling for a couple of extra houses

do not believe those who said that world was always like that

we probably reached the peak in societal decency in the 1970s, in the West, and it is going backward, almost medieval now, ever since