Is this as good as it gets? One and a half days into the new month, and the portfolio is already up a percent and a half, with all components making money. For a natural worrier like Macro Man, this is enough to set the alarm bells ringing. When everything goes up at the same time, it often smacks of complacency. To paraphrase Yoda, happiness leads to complacency; complacency leads to greed; greed leads to hubris; and hubris leads to the dark side of fat-tailed corrections.

It would of course be churlish to suggest that Friday’s data was much of anything but bullish for risky assets. Somewhat stronger than expected growth data combined with a lowball reading on core PCE (which came back to the top of the comfort zone for the first time in more than a year) is a virtual dictionary definition of risky asset Nirvana.

Yet beneath the surface, worries still persist. Chinese equities remain firmly on the back foot, with Shanghai A and B shares both down 8%. While the year-to-date readings remain firmly in tasty territory, the failure to rally in line with Western markets’ Friday performance, combined with some rumblings on forthcoming tightening measures for property, remains a source of concern. Lest we forget, China (and Russia) is the straw the stirs the global liquidity drink (as prepared by Ken Kesey?); further domestic tightening could eventually find its way to the rest of the world.

Of course, PBOC is not the only game in town, and plenty of other central banks have wood to chop. This week alone could potentially see tightening in New Zealand, the UK, and Eurozone. In the US, meanwhile, the strip has now priced out virtually any chance of an easing. Given the revival in the recent activity data, is it too early to begin contemplating market pricing of a further Fed tightening? Perhaps. But if housing ever leaves the front page of the financial market tabloid, the chances of a tightening may be closer than is commonly believed- particularly if sequential monthly inflation readings pick up again (of course, there’s no guarantee that they will.)

Of course, PBOC is not the only game in town, and plenty of other central banks have wood to chop. This week alone could potentially see tightening in New Zealand, the UK, and Eurozone. In the US, meanwhile, the strip has now priced out virtually any chance of an easing. Given the revival in the recent activity data, is it too early to begin contemplating market pricing of a further Fed tightening? Perhaps. But if housing ever leaves the front page of the financial market tabloid, the chances of a tightening may be closer than is commonly believed- particularly if sequential monthly inflation readings pick up again (of course, there’s no guarantee that they will.)

What will it mean for risky assets? To paraphrase a recent poster, not all tightenings are created equal, and as long as credit remains tight there need not be cause for alarm. Macro Man would broadly agree with this view and admit that the current rise in interest rates has been of the ‘good’ kind. Yet all good things must come to an end, and if current trends persist for another few weeks, month end could well see a tasty asset allocation rebalancing out of equities and into fixed income from pension funds.

What will it mean for risky assets? To paraphrase a recent poster, not all tightenings are created equal, and as long as credit remains tight there need not be cause for alarm. Macro Man would broadly agree with this view and admit that the current rise in interest rates has been of the ‘good’ kind. Yet all good things must come to an end, and if current trends persist for another few weeks, month end could well see a tasty asset allocation rebalancing out of equities and into fixed income from pension funds.

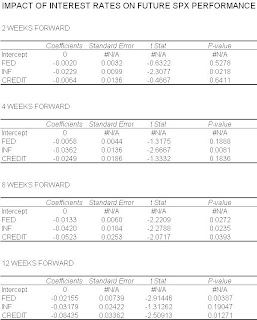

In any event, Macro Man was curious to see if he could identify whether different kinds of tightening matter. He therefore constructed a simple study to find out. For a sample period dating back to the beginning of 2002, he looked at:

* Fed tightening expectations, as measured by the difference between the second and fourth Eurodollar contracts

* The two month change in 10 year inflation breakevens

* The two month change in credit spreads

He then regressed these inputs with the subsequent change in the S&P 500 over a variety of time periods. The results were rather interesting.

All coefficients had the right sign, i.e. negative (indicating that higher rates lead to lower stock prices and vice versa.) But he found quite a remarkable disparity between which rates matter for stocks at various time periods, as defined by a t-statistic and p-value.

All coefficients had the right sign, i.e. negative (indicating that higher rates lead to lower stock prices and vice versa.) But he found quite a remarkable disparity between which rates matter for stocks at various time periods, as defined by a t-statistic and p-value.

In short run (less than a month) time periods, inflation breakevens exert far and away the most (and indeed, only) significant influence on stock prices. Macro Man was pleased to see this result, as he has often flagged breakevens as a key point to watch. Importantly, breakevens are currently giving the all clear for further solid gains in stock prices.

One an eight week horizon, each of the three rate measures appear significant, with t-stats above two and p-values below 0.05. Twelve weeks out, breakevens cease to carry statistical significance while Fed expectations and credit exert a stronger influence than they do over shorter time frames. Given that all three inputs are currently mildly supportive of equities, despite the recent run-up in govvy rates, perhaps the current environment really is as good as it gets.

(Disclaimer: this was not an exhaustive study, and Macro Man understands that varying/optimizing independent variable time lags could yield more substantive results. This could perhaps be a project for some point in the future if and when he has the time.)

It would of course be churlish to suggest that Friday’s data was much of anything but bullish for risky assets. Somewhat stronger than expected growth data combined with a lowball reading on core PCE (which came back to the top of the comfort zone for the first time in more than a year) is a virtual dictionary definition of risky asset Nirvana.

Yet beneath the surface, worries still persist. Chinese equities remain firmly on the back foot, with Shanghai A and B shares both down 8%. While the year-to-date readings remain firmly in tasty territory, the failure to rally in line with Western markets’ Friday performance, combined with some rumblings on forthcoming tightening measures for property, remains a source of concern. Lest we forget, China (and Russia) is the straw the stirs the global liquidity drink (as prepared by Ken Kesey?); further domestic tightening could eventually find its way to the rest of the world.

Of course, PBOC is not the only game in town, and plenty of other central banks have wood to chop. This week alone could potentially see tightening in New Zealand, the UK, and Eurozone. In the US, meanwhile, the strip has now priced out virtually any chance of an easing. Given the revival in the recent activity data, is it too early to begin contemplating market pricing of a further Fed tightening? Perhaps. But if housing ever leaves the front page of the financial market tabloid, the chances of a tightening may be closer than is commonly believed- particularly if sequential monthly inflation readings pick up again (of course, there’s no guarantee that they will.)

Of course, PBOC is not the only game in town, and plenty of other central banks have wood to chop. This week alone could potentially see tightening in New Zealand, the UK, and Eurozone. In the US, meanwhile, the strip has now priced out virtually any chance of an easing. Given the revival in the recent activity data, is it too early to begin contemplating market pricing of a further Fed tightening? Perhaps. But if housing ever leaves the front page of the financial market tabloid, the chances of a tightening may be closer than is commonly believed- particularly if sequential monthly inflation readings pick up again (of course, there’s no guarantee that they will.) What will it mean for risky assets? To paraphrase a recent poster, not all tightenings are created equal, and as long as credit remains tight there need not be cause for alarm. Macro Man would broadly agree with this view and admit that the current rise in interest rates has been of the ‘good’ kind. Yet all good things must come to an end, and if current trends persist for another few weeks, month end could well see a tasty asset allocation rebalancing out of equities and into fixed income from pension funds.

What will it mean for risky assets? To paraphrase a recent poster, not all tightenings are created equal, and as long as credit remains tight there need not be cause for alarm. Macro Man would broadly agree with this view and admit that the current rise in interest rates has been of the ‘good’ kind. Yet all good things must come to an end, and if current trends persist for another few weeks, month end could well see a tasty asset allocation rebalancing out of equities and into fixed income from pension funds.In any event, Macro Man was curious to see if he could identify whether different kinds of tightening matter. He therefore constructed a simple study to find out. For a sample period dating back to the beginning of 2002, he looked at:

* Fed tightening expectations, as measured by the difference between the second and fourth Eurodollar contracts

* The two month change in 10 year inflation breakevens

* The two month change in credit spreads

He then regressed these inputs with the subsequent change in the S&P 500 over a variety of time periods. The results were rather interesting.

All coefficients had the right sign, i.e. negative (indicating that higher rates lead to lower stock prices and vice versa.) But he found quite a remarkable disparity between which rates matter for stocks at various time periods, as defined by a t-statistic and p-value.

All coefficients had the right sign, i.e. negative (indicating that higher rates lead to lower stock prices and vice versa.) But he found quite a remarkable disparity between which rates matter for stocks at various time periods, as defined by a t-statistic and p-value.In short run (less than a month) time periods, inflation breakevens exert far and away the most (and indeed, only) significant influence on stock prices. Macro Man was pleased to see this result, as he has often flagged breakevens as a key point to watch. Importantly, breakevens are currently giving the all clear for further solid gains in stock prices.

One an eight week horizon, each of the three rate measures appear significant, with t-stats above two and p-values below 0.05. Twelve weeks out, breakevens cease to carry statistical significance while Fed expectations and credit exert a stronger influence than they do over shorter time frames. Given that all three inputs are currently mildly supportive of equities, despite the recent run-up in govvy rates, perhaps the current environment really is as good as it gets.

(Disclaimer: this was not an exhaustive study, and Macro Man understands that varying/optimizing independent variable time lags could yield more substantive results. This could perhaps be a project for some point in the future if and when he has the time.)

3 comments

Click here for commentsWith the Nazz leading the way, U.S. stock market action finally showing strong signs of being the real thing rather than the grudging, overly-hedged climb along the route of least resistance that has mostly characterized it since, say 2004.

ReplyThat it is happening in the face of failing bond prices and a resilient VIX might indicate that we are entering the more familiar terrain of unrepentant speculation.

Welcome back!

CB

Call me old-fashioned and ignorant and closed minded, but should people give a crap about the Nazz these days? Looking at the index weights, the 3 biggest components (MSFT, CSCO, INTC) are erstwhile supergrowth high-fliers whose recent business fortunes appears to have denigrated them to cash-cow status- hardly the stuff of untrammeled speculation.

Reply(And as a pedantic aside, the Nazz is up less than the SPX or Dow this year, particularly when dividends are added in.)

I'm not sure we disagree. It's awfully easy to argue that those three components are historical artifacts that distort what remains an essentially speculative market and any information that might be gleaned from it.

Reply