Equity markets took a standing-8 count over the weekend and came out swinging on Monday, bouncing roughly 1.5% off the lows from Friday’s close, and a solid 4-5% off the spike bottom lows around lunchtime.

Friday’s headlines were notable given the change in sentiment--a correction! To again quote Matt Levine at Bloomberg….”there you go. All you’re stock prices are correct now.” The rest of the financial media howled in unison.

It wasn’t a contrarian green light, but it was close. Buyers had a few strong points in support:

- On the technical side, there’s little doubt a significant portion of the price action last week was driven by some combination of forced selling, negative convexity, liquidity seizures, and outright panic.

- Fundamentally, no change, and notably cheaper valuations:

- still strong global growth,

- A weak USD

- Strong commodity prices

- Fiscal stimulus in the US

- A new Fed chair that has pledged fealty to the credit-addict that gave him the job

- Moreover, central banks that recognize the fragility of the beast they birthed

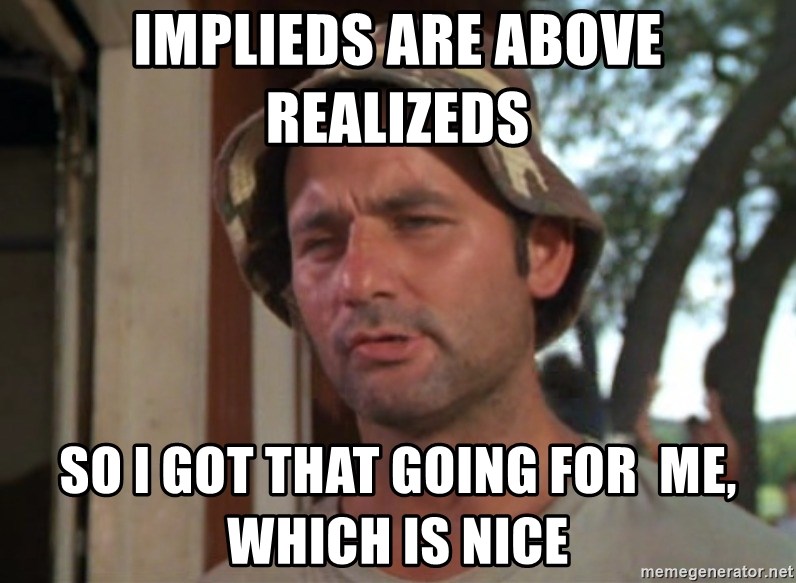

An astoundingly quiescent market, followed by higher rates and a modest risk-off move in stocks, contributed to a MOAB move in vol, gamma and the VIX. Usually when something like this happens--and it is supposed to happen periodically--vol everywhere spikes higher, FTQ assets appreciate, and the system rebalances itself.

What is not supposed to happen is something like this:

So what’s going on? There’s been no shortage of media coverage on the blowup of short vol ETNs like XIV. But as I highlighted last week, these products are--or were anyway--$2-4bn in notional value in a market that is many, many times that size.

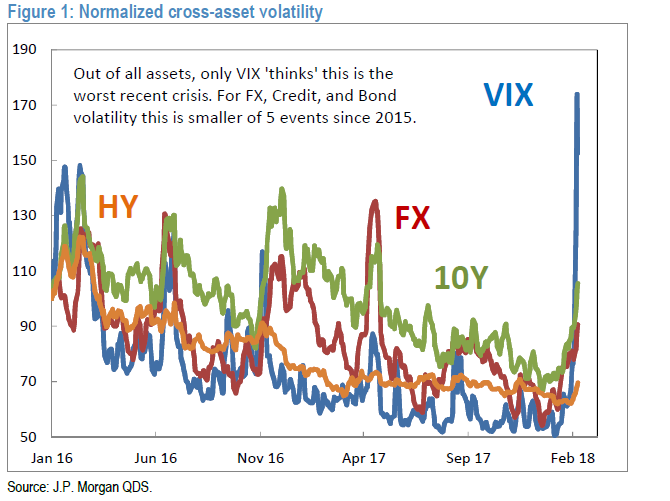

The real iceberg beneath the surface is the short-vol trade writ large. The short-vol trade goes by a few different names--last October, in an article highlighting the depths of the short-vol monster, Chris Cole at Artemis Capital Management illustrated it as a pyramid:

Cole called this the Ouroboros, the mythical greek snake that devours itself by eating its own tail.

“Volatility as an asset class, both explicitly and implicitly, has been commoditized via financial engineering as an alternative form of yield….A long dated short option position receives an upfront yield for exposure to being short volatility, gamma, interest rates, and correlations. Many popular institutional investment strategies bear many, if not all, of these risks even if they are not explicitly shorting options….Lower volatility begets lower volatility, rewarding strategies that systematically bet on market stability so they can make even bigger bets on that stability. Investors assume increasingly higher levels of risk betting on the status quo for yields that look attractive only in comparison to bad alternatives.”

Put another way, as the avalanche of monetary stimulus compressed risk and pushed down expected returns, Wall Street needed a new asset class to sell in the search for yield. Pension funds needed to maintain high returns, and were ready to listen to the sales pitch for volatility as an asset class.

Let's look back a couple of years for some examples of how this was sold to investors. Pimco led the charge in 2012 with this article entitled, “The Volatility Risk Premium.”

“We conclude that the risk-return tradeoff for volatility strategies compares favorably to those of traditional investments such and equities and bonds and that the strategies exhibit relatively low correlations to equity risk.”

Ooh, now you have my attention, says Joe Capital-Allocator at XYZ Pension Fund, tell me more. All too happy to oblige, Pimco continues:

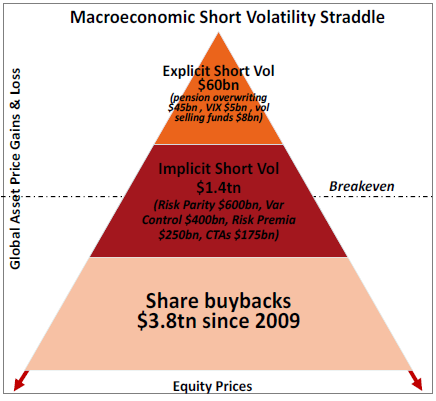

Well there it is...implied vol is typically higher than realized vol. Real MIT rocket science PhD type of stuff. There is a good rationale and justification for that “premium” that is not unlike an insurance premium. Though I wouldn’t call it that, since realized and implied volatility really don’t have a relationship other than one that is backward looking.

Yes, there is a “price” there. What’s the right price? Think back to 2012--in the article The Pimco authors concluded, “given the economic rationale for the existence of a volatility risk premium, and the supportive supply-demand situation that emerged following the 2008 financial crisis, we believe an allocation to volatility strategies could enhance portfolio efficiency.”

Yes, there is a “price” there. What’s the right price? Think back to 2012--in the article The Pimco authors concluded, “given the economic rationale for the existence of a volatility risk premium, and the supportive supply-demand situation that emerged following the 2008 financial crisis, we believe an allocation to volatility strategies could enhance portfolio efficiency.”

I’ll bet they did….but they were right! Back in 2012, there were no shortage of Black Swan disciples of Roubini and Taleb pitching and building tail risk products and funds. The memories of the GFC were still fresh, and the wounds were still healing. If that weren’t enough, the entire European project nearly imploded on itself, giving more ammunition to those that believed the financial system was on a steep descent into (further) chaos. It comes back to recency bias...The demand for volatility was high. The short-vol trade was born to provide the supply...and fees!....to support it....and yield-hungry institutional investors ate it up. It was a good trade if you had a long-term time horizon and didn’t think the world was about to end.

The trouble is, someone forgot to turn off the machine. By 2015, Nomura was pitching a product they called the eVRP--the Equity Volatility Risk Premium-- all backed by a Nomura index that followed this kind of thing. As prices rose, financial engineering took over for thematic simplicity.

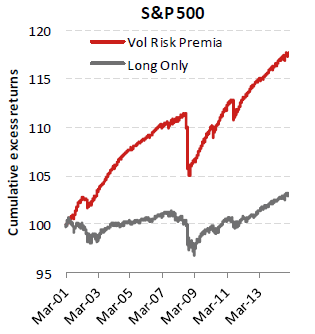

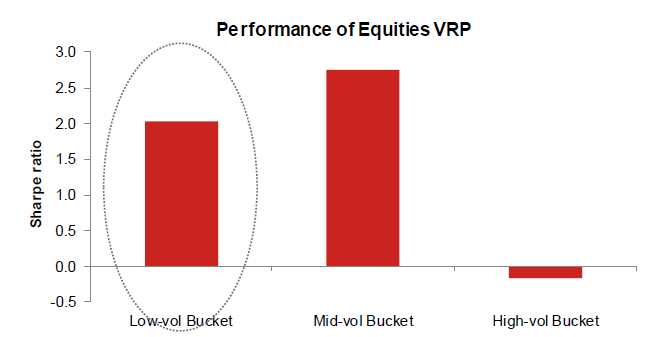

Now, this wasn’t just a diversifier, it was some sexy stuff! Check out these charts:

The volatility risk premium has been a great trade compared to “long only”

Selling equity vol risk premium is when vol is low...your road to a 2.0 Sharpe

The equity vol risk premium is better than ya know, other stuff

All the cool kids are doing it

Three years on from the Pimco article, when there was a tasty volatility premium thanks to the back-to-back existential crises in global markets, Nomura is pushing the same trade, only in the form of their esoteric eVRP product rather than the more straightforward Pimco strategies of 2012. And of course, Nomura has the data to back it up, and your friendly salesman has just the right product for your long-term risk bucket.

This is the Ouroboros. Just like the housing/credit bubble in the mid-00s, the financial system doesn’t know how to stop. Just because there was a rich volatility premium in 2012, doesn’t mean it is perpetually and always going to exist. In fact...quite the opposite. As markets calmed, the trade worked….and more money flowed into it. Supply and demand swung the opposite direction, but nobody ever turned off the machine.

The snake latched on to its own tail, compressing vols, perpetuating BTD, which compressed vols, which juiced returns. Lather, rinse, repeat. And wait for the bonus checks to roll in.

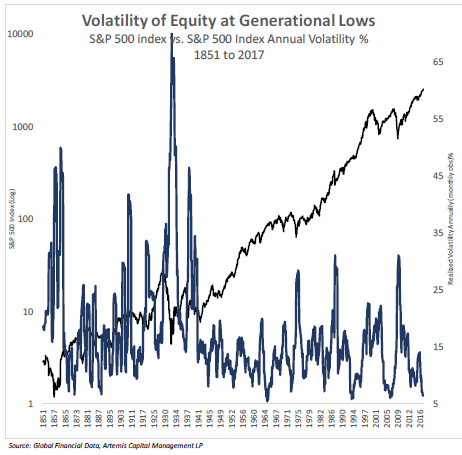

How can you identify when this trade is overdone? You can probably point to your own examples, but these two charts sum it up:

You’re telling me there’s an equity volatility premium….even as equity vol its generational lows?

That can only be because you’re looking at realized vol still below implied vol. That’s what you call a “premium”?

Then in fixed income….monetary authorities are finally hiking rates and decreasing or stopping asset purchases….and you think you can capture a “premium” for volatility above realized when implieds (as proxied here by 1m/10y USD swap vols) are THIS far below the long-term average?

(I trimmed this chart back to the lows in January before the spike in the last two weeks to illustrate the point, but the current level stands just above 80)

As Cole said in the “Alchemy of Risk” article...as the short-vol sales machine perpetuated itself, it gave birth to a reflexive process:

“What we think we know about volatility is all wrong….Modern Portfolio theory conceives volatility as an external measurement of intrinsic risk of an asset….this highly flawed concept, widely taught in MBA and financial engineering programs, preceives volatility as an exogenous measurement of risk, ignoring its role as both a source of excess returns and as a direct influencer on risk itself. To this extent, portfolio theory evaluates volatility the same way a sports commentator see hits, strikeouts, or shots on goal. The problem is volatility isn’t just keeping score, but is massively affecting the outcome of the game itself in real time. Volatility is now a player on the field. “

That’s what has changed...Pimco and Nomura built their analysis on a history where volatility was a measure. Now it is a player. It has a price. What once was rich is now obscenely expensive.

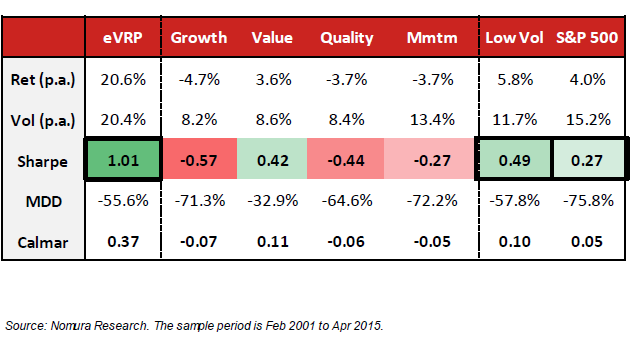

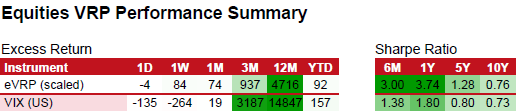

Yet for these guys it all comes back to returns--more specifically risk-adjusted returns. How did the Nomura guys fair at selling volatility?

This is the stated performance of their “eVRP” product as of January 25:

12-month excess return of 4716 basis points! A 1yr sharpe ratio of 3.74! As Kevin Muir at MacroTourist said back in November in a post on the same subject, “Hedge fund managers do terrible unspeakable things for Sharpe Ratios of 2.5 to 3. Indeed...and pension fund investors are no different. Moreover, that 5-yr Sharpe of 1.28 is pretty spicy too when compared to the Sharpe on long-only equity returns skulking on either side of .5.

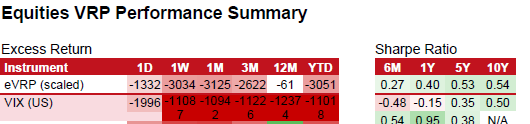

Now, fast forward to last Thursday:

Oh dear. Our precious short-vol baby vaporized that 1yr excess return in only two weeks! And those Sharpe ratios went from heavenly to downright ordinary, and I’ll hazard a guess that these figures aren’t including the tasty fees that your pension fund paid their friendly neighborhood bank or hedge fund for managing this risk over the past few years.

It started as a good trade...but as the money rolled in, they just couldn't turn the machine off.

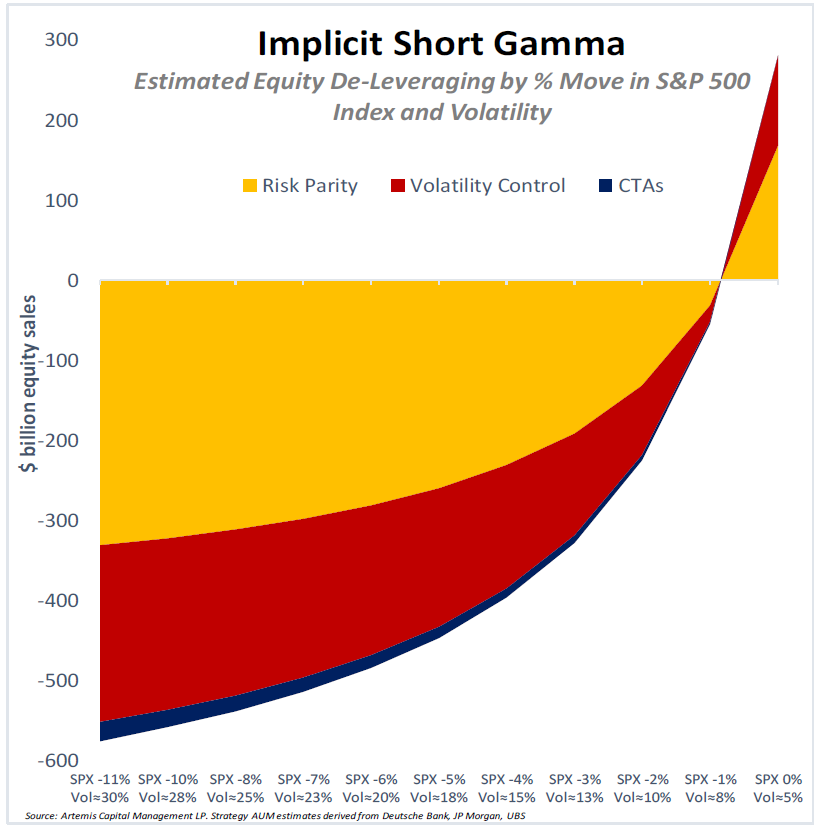

And so it begins, where the top of Cole’s short-vol pyramid has gotten wiped out--the $60-$100bn in explicitly short-vol funds that were betting on pension fund overwriting, “risk premiums”, or just whacking bids in the VIX. While these funds may not have blown up in style like XIV, they have been mortally wounded by the combination of a landmine in their performance record and the demonstrable gap in liquidity for their strategies. The universal risk management strategies like VaR de-risking like those discussed by Polemic in his weekend posts will play a big role too.

Nevertheless, for short-vol the sales pitch is dead--these strategies won’t go away overnight but they will die a slow death. In the short-term, vol will subside--but the next chapter hasn’t been written yet. What does the future hold for the more subtle short vol strategies--like “volatility control” and risk parity?

That might depend on faith in the system, the continued negative correlation of equities and fixed income products, and the ability of leveraged corporations to continue servicing their debt in the event of a shock to the system or a material slowdown in global growth. And don’t forget this….liquidity is now such that this short-gamma trainwreck may not be so easily contained within equity markets when we inevitably encounter a genuine exogenous shock to the system.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

48 comments

Click here for commentsGreat post, Shawn. Always the engineers seem to miss the reflexive aspect of markets, whether for houses, or in this case, volatility.

ReplyLove how those 10-year Sharpes went to mediocre in a week. That's all it took to go from hero to zero.

Does it matter who holds the bag when the other shoe drops? Back in 2008 banks were selling truckloads of long-dated vol to clients without the market to hedge in. That was vega not so much gamma, still back end vol when up a lot, and short dated gamma hedges rolled off, and there was a risk manager who was mentally wounded, meaning that - no, you couldn't sell more vega even if there was a bid. Fast forward, there was a supply of gamma, which could have been hedged or was not hedged. In the first case the risk was distributed and net result outside var computation is nill or in the second case market makers in short gamma products / banks lost a lot in carry and may have made some back on the last move. Either way vol is vol, gamma is gamma, both are tradable, numbers will be changing. I can't see anything new. Potentially a regime change and that's it. Anything else is just news and news is old.

ReplyMoreover, human nature is to be shot gamma and vega. Bulge bracket bank (when that was a thing) management meeting: Who was this guy who sold varswaps to us when we ran for cover? That was the guy who was fired by us in a first place for being short variance.

ReplyAll that is to say, it was very quiet for a very long time, something mildly exciting but not extraordinary happened, normalisation is good, is there anything else to read into? Welcome two way market.

ReplySuperb post Shawn thank you.

ReplyGreat comments Nick.

I guess the problem arose, like most problems in financial engineering, where a zero sum game is played but all the players are convinced they are winning. A phrase I once used at a credit meeting in 2007 when our credit traders told us that everything was great because it was hedged through a AAA monoline.

And Vegas was just a reasonably priced bar tab for those credit traders, otherwise it's too much effort. We can easily move to moral aspects of selling short gamma products to quasi retail, but I don't find those much different to commodities prospecting (how about a Yorkshire dales mine?) or penny stocks. Nothing new under the sun.

ReplyWhile I am at it, could prohibition of any kind of management fees and bid ask spread go a long way for 'investor' protection? One choice price on the screen, any advisor or consulting shares performance? Has that ever been tied?

Reply@Nick--that's pretty much the point--nothing new under the sun. Just a different product at the center of this leg of the credit cycle. And while it is true that this is simply the return of a two-way market, it should not go unnoticed how big the move was relative to the really boring news/information that triggered it. Another chart in Cole's piece was the reaction function of implied vols to moves in the S&P over different market regimes in the past thirty years--in years past it was a relatively linear relationship, but now it is far more inelastic--a much smaller move in the S&P triggers a much bigger move in vol than ever before. Several other changes in market structure appear to be contributing to that as well.

ReplyCall me crazy, but is anyone else suspicious of the timing of the ViX blow up, happening at the same time Yellen departs? If the conspiracists are correct, and the Fed has been selling volatility all along, perhaps the new Fed chair wasn't comfortable with this arrangement and shut it down as a condition of his taking office?

ReplyPerhaps far fetched, but certainly possible. As a thought experiment, consider the implicatiins, if this were true.

Where would this show up on the Fed's P&L? They would have had to have taken one hell of a haircut this month.

Nikkei selloff is a nice reminder that when your market is full of exporters and your currency is cheap versus PPP, you might want to adjust earnings for a revaluation to PPP before concluding the market is "cheap."

Reply@Skr: to answer your comment from the last post...

ReplyHunt differentiates between facts and story. Imo facts is what counts in the long run (as you also said), but the short run is story driven. Now, he may be right or not, I don’t know. What I find interesting, though, is that all of a sudden every pundit and his grandma talk about inflation and why there is nothing to worry about.

Rising inflation expectations were my most likely culprit to upset the QE apple cart. Because nominal long term rates go up, as simple as that. A significant part of the current market edifice seems to be built on the assumption that (nominal) rates stay low for a very long time (equities attractive relative to bonds, hunt for yield, you name it). Rising rates, at least in the short term, could be the catalyst to start the unraveling.

But then i could be completely wrong, of course.

Fantastic post. A post mortem is especially interesting when there has been a pre mortem discussion of the body here too!

ReplyInflation fears (?hopes?) of punters are way overblown. US wage blips don’t really matter a great deal to prices when most things are actually being made in China, Vietnam and Mexico. Crude oil has the potential to re-enact the swoon of 2014, as long positioning meets growing US supply. The price of crude is a huge global inflation driver.

This episode continues to remind one of the faux recovery of 2010, when momentum traders were out in force, and thanks to those Treasury shorts you could buy a US10y yielding 4% – what a great trade that turned out to be. A classic summer slowdown followed, complete with a Flash Crash and a lot of losses for punters long the reflation trades. QE2 followed. The long bond appreciated >20% from its April/May nadir. Something similar could happen here, if not this month then next. Crowded trades always burn the late arrivals, e.g. short volatility…

If US10y screams to 3% there will certainly be more unwinding of "implicit short vol" strategies, however….

Keep an eye on high yield. It has, thus far, made a very weak Dead Cat Bounce. HY often reflects acute funding difficulties in the economy that are not always apparent in the large cap space, which is why we would be short small caps at some point.

Seems to me that this was classic relative liquidity in action. Relative liquidity in pure vol plays vs straight equities. Equity markets crash down, they don't crash up. Vol on a move lower is a beast, So, the equity market starts a move lower (finally?) on more talk of higher rates/inflation, realized vol starts to pick up, short vega - ditto gamma of course - needs to be covered. Buy vol. The move continues, liquidity isn't there in enough size in vol but is enough in SPY, sell the underlying market as a proxy, which pushes that market lower which squeezes the vol players and your position spirals down the drain. What happened when the vol positions were pronounced dead? I bet CSFB bought back their short SPY etc on Friday.

ReplyA nice dissection of longer-term inflation trends and dynamics here:

Replyhttps://viableopposition.blogspot.ca/2018/02/solving-federal-reserves-inflation.html

So many headwinds for Reflationistas: Demographics. China. Amazon. US shale. The list goes on and on.

Looks like that was the CPI "beat" that the market expected, more or less. A 3.0 handle for the y/y might have caused some more carnage, especially in USTs. Let's see if TY and US can rally on "bad news" today.

ReplyRetail sales fell…. the cure for higher prices is higher prices, especially for "apparel", LOL. Seriously? Apparel? Must be the Melania Trump factor stimulating that sector. Millennials are still shopping at the thrift store.

Note that equities are being sold harder than bonds here. This isn't playing out like a RP meltdown day. Equity dip buyers and trapped longs must feel uncomfortable here but I doubt this amounts to very much.

This was always going to be a difficult day to trade and we're glad we sat on our hands today. Another dead cat bounce lies ahead of us, into the monthly expiration. Vol selling will probably be the most profitable day trade.

@LB I haven't dug around in the CPI print yet but hearkening back to my post on US inflation last fall, medical costs and cell phone expenses have been big drivers, both up (drugs, in 2016) and down (both, in 2017). Goods CPI has been low vol. Energy the big x-factor as always. Just guessing, but I think this is pretty much what the fed has been telling us for a while. The piece you linked to highlights this excellently, can't remember if I highlighted that pro-cyclical/anti-cyclical trend or not...but I do remember reading that paper from the fed!

ReplyRe: VIX...cracking back to 20, obviously the market has wrung out some event risk post-CPI--seems like the 1st battle is over for now.

Re: JPY, interesting this one has chosen now to start running--bbg and wsj claiming "risk off causing short yen carry trades to unwind." I call BS on that explanation-- my thesis on higher growth and greater probability of a tapering of asset purchases sooner rather than later seems more apt given rising rates putting more (or less, i guess) pressure on the BoJ's rate control corridor. But the weak GDP # not giving a whole lot of confidence to the local story. If I were sitting in front of a bbg terminal right now I'm sure I'd hit the till on long JPY here but still like it in the context of the global growth story.

A shout out for Shawn's well-timed post on USDJPY earlier this year! Nicely done.

Replythanks johno....

Replywsj out this morning with a related article---I spared blasting a couple of individual funds that I saw had new allocations to these strategies. The consultant industry sells the same product to all of them--I can assure you more than 60 out of 6000 funds are into this kind of thing.

https://www.wsj.com/articles/pensions-and-endowments-gambled-on-market-calm-then-everything-changed-1518626836?mod=e2tw&page=1&pos=1

the buried lede....Harvard owns 100,000 shares of SXVY? I'd love to know if Harvard still has that 100,000 shares.... It's always the unsophisticated mom-and-pop investors that are left holding the bag.

Very well done. The spread between implied and realized did not provide an early warning of a regime shift. However, the simple break of a very LT down trend did provide a bit of smoke and the hint of fire. The problem with the sale pitch or rather the part that was a bit disingenuous was the idea that this was a premium that was somehow embedded in the market which is certainly not true. They were packaging an what was a "trade" and trying to turn it into an investment, which of course it is not. And of course, no mention of the asymmetric risks of being short vol vs. being long. (bleed vs. blow up)

Reply@Shawn, I believe that was my message on the day of - poor folks got hurt.

ReplyAlmost surreal to see all trades working, RBOB, TLT, DXY. What a sharp focus would do!

I am going to take a break, guys, will start posting again after I see this place cleaned up. Regulars deserve better than that...

Sorry, Shawn :(

Isn't it funny when equities shrug off the CPI print, and the Dow reverses up +600pts in a few hours... funny also that all the permabears & know-it-all's have either disappeared or run away crying :)

ReplyPlus ça change, plus c'est la même chose...

@Buy Stocks, have we to listen to the "same old, same old" (lol) all the time? What happens next, just in equities of course?

Replyyou're wrong about permabears. Al Edwards was on the tape this morning, confident as ever. And fresh out of a dinner with Bob Junjuah.

ReplyBuystocks, you are so right. I have been stopped out and gone long at 2690. Where should I put my stop? I'm playing this on a one week view Thanks.

ReplySkr - What happens next is stocks go higher (look, the Dow is already up almost +100 points since you posted 10 mins ago).

ReplyShawn - Gotta love Al; wrong on every single prediction. Class.

Polemic - You seem to be buying the rally, not the dip. Try it the other way 'round.

@IPA, shame that only one internet trol chased you away

Reply@Buy Stocks(lol), you maybe right, I have not been this strung out (scalping), since your Mam(Linda?) caught me with her porn collection! Please turn the machines back on, so I can get them old images out of my mind.

ReplyThe really important "inflation" data is not US CPI but the EU number, due Feb 23. That controls the prospects for early QT by Draghi. Let me give you a clue, EURUSD too strong, EU inflation fading - QT is NOT HAPPENING. Cue a sharp dollar rally.

ReplyThree over-extended crowded trades becoming even more over-extended today: Short USTs. Short DX. Long €. Expect all of these to reverse, perhaps as soon as next week.

Buy Stocks, Mr Market is just "Fib-ing" here. Target zone around SPX 2750. Exit Rally in progress? A bull trap for noobs...

Leftback - Maybe, but I think we re-visit ATHs.

ReplyLook guys there are 2 possibilities:

1) The US and world economies are booming, finally casting off the shadow of the GFC...

2) We have kicked the can down the road via huge injections of liquidity, debt levels are exploding and we are on the brink of the abyss...

Now let me share with you a secret: in both scenarios, equities surge higher!

in 1) Booming economy, PE up etc, stocks rise; in 2) CBs & govts shit themselves, and do all in their power to support equities etc to keep retirement funds & the financial system stable.

See, macro is easy :)

Btw - about that fishy apparel inflation data? I ridiculed this immediately, and Bloombags is all, like, people have to buy clothes:

Replyhttps://www.zerohedge.com/news/2018-02-14/apparel-inflation-hits-67-year-high

Quite normal... c'mon, FFS!!.... this isn't Stalinist Russia or China's magic number machine - STOP MAKING UP THE DATA!

{"Hello... yes Mr Stalin... I am sorry, I didn't know. Oh, you're on LinkedIn? Good! Yes Joey, I'd be delighted to connect with you.}

"f*ckwits" my friend is lame!

ReplyAnytime, anywhere.... As your Mam used to say,is the truth.

Can you please advise, how one should address you for future reference?

Indeed sir.

Reply@Mi Pa, I am not leaving because of the troll. I am leaving because of the blog administrator's inability or lack of desire to clean up the house. I am busy enough trying to navigate the markets, I don't need daily distraction and useless noise to take away my precious focus. I caught myself wasting time on reading the insults and taking things way more seriously than I should. I refuse to remain in the room full of bright people who are constantly offended by one unruly imbecile. I completely disagree with the notion that he should be left alone and continue to be ignored while he is allowed to call all macro traders, central bankers, and basically every person who disagrees with him a f*ckwit. This is the kind of ignorance and lack of respect that I witness in all facets of life and I am too overwhelmed by it everywhere else to be reminded of it here as well.

ReplySo long...

@IPA, well i am truly sorry about that, i love to read your posts.

ReplySorry to see you go. IPA.

ReplyPersonally I don't worry about insults from Buy Stocks, 12 y-o HFM etc and I think many of us here enjoy the late night mescaline-fueled insights of Amps. I don't know Mrs. Buy Stocks Sr., but I am sure that she is a very nice lady.

Back to the markets and LB's new theme for next week: SHORT EURO. If you want to, you can go full Dalio and short DAX etc.. but we prefer to play this via FX. Simply, EURUSD 1,25 means German companies make no money. There will have to be some back-tracking on the QT hints from Draghi, or else the EU inflation data will do it for him. Long EURUSD is very crowded here.

In the US we think the short USD, short UST complex may be the next crowded trade to crack (partly in synch with the above).

A retrace of the Spoos was predictable into options expiration, and what we are seeing here looks textbook. We'd be inclined to play US equities from the short side next week, especially the small caps - look at the continued weakness in HY.

As for vol, the short vol ETFs may have expired but the thematic short vol community is still out there, in the form of passive equity longs and the JBTFDers. The volatility itself is not over, and that means more pain ahead for someone.

LB

ReplyRegardless of ho you or I might think this inflation issue works out in the longer term there is absolutely no doubt that momentum is shouting yields are rising, rate sensitive stocks are falling, corporate debt is adjusting to duration mismatches. Re the latter it's not surprising because yield chasing trumped interpretation of low for longer perhaps because at the time fiscal policy wasn't really seen as coming. As for over crowded we've seen these situations stay loaded for longer than it is comfortable to fight the current. All the signs are inflation matters to current positioning.

So does anyone have a strong opinion on the notion that, since the S&P didn't break its 200-day moving average, a re-test of the recent lows is almost a given in the next few weeks?

ReplyGus - You surely mean a re-test of ATH's?

ReplyAs I predicted, BTFD worked a charm again today and equities pushed higher (Nasdaq up almost +1.5% on the day). I expect more snowflakes to run away from this blog in tears...

We'll soon be back to ATHs and the endless grind upwards. Enjoy!

Ok listen up Buy Stocks and the rest of you: per IPA's point above, I've spent precious time going through this comment thread and deleting anything that is 1) aggressive towards other users, 2) vulgar, INCLUDING using curse words with asterisks, 3) just generally disrespectful, or anything you wouldn't say in good nature if we were all shooting the breeze about markets over pints in a pub.

ReplyI'm going to give you my Dad speech here--I thought you were old enough to handle the responsibility of an open forum but you've proven me wrong. I'm going to wield the ax accordingly for the foreseeable future.

If you want to blast people, go to zerohedge. The people that come to this blog are here *because* they don't want to be a part of that.

For me, I contribute to this blog *because* of the discourse in the comments section with bright people. I wouldn't spend the time writing this stuff if I were just shouting into a canyon. Please show a little respect to me and the others in this forum by keeping it respectful.

@Gus: Yes. Abso-freakin-lutely. This week has played out like the classic retrace into options expiration, as predicted.

Reply@Buy Stocks: Respectfully, squire, I am going to pretend that you are a parody poster. I wish that were true. No tears in trading, btw!

@checkmate: All eminently reasonable, but look, sentiment and positioning are extreme in USTs and EURUSD. We saw what happened with equities and vol. If I am wrong on this - well, I will get stopped out, and unemotionally set up and get ready to do it again. That's what happened with the short vol trade until finally we scored big.

A drop in future US inflation is already embedded into next month's price data with the recent pullback in WTI, which as of yesterday had pulled back >10% from its highs, this IN THE FACE OF MONTHS OF DOLLAR WEAKNESS. Gasoline will follow, those are important inputs into US PPI and CPI. This stuff isn't really very complicated. The growing US supply glut means a repeat of 2014 would not be a shocker. Take a look at what happened to yields during that oil market meltdown!

Because you are not in the US, you may not see and feel the US economy and inflation the way that we do here, especially as it affects middle class Joe and Josephine Sixpack. Believe me, the price of gasoline is important to EVERYTHING.

Leftback, the facts remain that SPX has had 5 green days in a row. The market is pushing higher, and most of the posters here have been wrong. I rest my case.

ReplyRe: oil/gasoline--the 2014 was supply, but 15 and 16 move was supply *and* demand. I think we've seen demand expectations back off a little in the move down in WTI, if that coincides with a continued acceleration in production we could be in for another leg down. But we'd need a big crack in global demand to supercharge that move lower. And you can figure out how the same sentiment/expectations game is playing out in bond yields.

ReplyImplieds are always trying to stiff you.

ReplySuch a informative blog. Day Trade is such a good thing and its good for income. If anyone interested in day trading. they should learn to trade the market

Replyinteresting counterbalance: https://www.bloomberg.com/news/articles/2018-02-20/buy-the-dip-isn-t-dead-in-fact-it-s-just-getting-stronger

Replyto this: https://www.bloomberg.com/gadfly/articles/2018-02-16/add-stock-buybacks-to-the-causes-of-the-market-downturn

Please join me today as I make impact, as you are planning for Christmas don't forget that their kids outside who are homeless that need help, I'm soliciting for your assistance today to join me as I plan to feed five children for this Christmas and I want to also send them back to school your support is needed nothing is too small nothing is too big for this purpose, if you are interested in joining me, email me at charitydonation8@gmail.com.

Reply

ReplyHas conclusively the ordinary impact!I figure you should check out support site.