To those in the US, welcome back from the most American of holidays. I’m sure there are other countries that have holidays largely devoted to gluttony, but as is often the case, America imported a good thing and made it better. Well, bigger and more gluttonous, anyway. Who else would have woven in nine hours of football and materialist retail bonanza into a celebratory feast day? Heck, now you don’t even have to drive to a retailer at sunrise and risk getting trampled to death to grab the best Black Friday deals. You can do it while sitting on the couch! Well done, America. U-S-A! U-S-A!

I’m back at my desk after a travelling for a couple of weeks and spending much of last week considering, buying and preparing my contributions to the Thanksgiving Day feast. The big story of the past two weeks has been the re-pricing of the front end of the curve in the US:

You don’t get a 30bp move in the 2y with the the 10y pinned in a 10bp range over a six week period without considering the message the market is sending to the Fed. Clearly there isn't much cooking in term premiums....the market hasn't lost faith in the lower natural rate, r*, or whatever you want to call it.

Which leaves us with this move in the front end, and what it all means. Please use the comment section to tell me what you think the market's message is...my two contributions would be 1) “there’s still a ton of liquidity out here”, and 2) “we don’t think the business cycle is sustainable, nor do we believe core inflation dynamics are going anywhere.”

Before this slips into another “curve shape” post, it is the second message I want to focus on. While there has been little evidence that “demand-push” inflation is outside what we might expect at this stage of the business cycle, the buried message is related to big increases in oil, gas, and fuel oil prices since early this summer. As much as they will tell you these prices are “transient” and thus don’t impact monetary policy, they will likely be tough to ignore in 2018 because they will hit consumers in the pocketbook and push headline inflation higher.

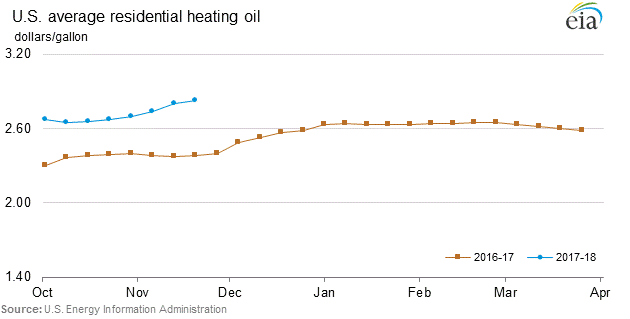

We all know what the crude chart looks like, with the move from the low 40s to the mid-high 50s in WTI, roughly a 30% move. There has been a similar move in residential heating oil:

And as we come into the heating season, prices are tracking well above last year:

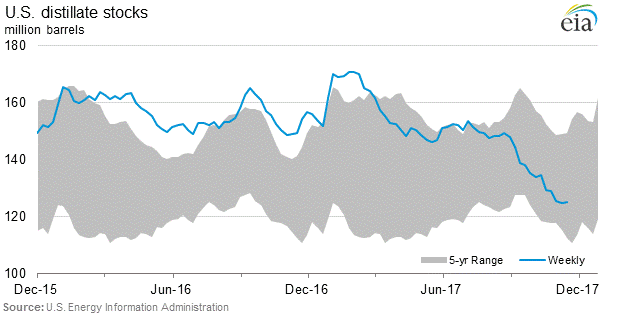

And inventories are approaching 5-year lows, which argues for big prices increases if we get a cold winter (that being said, I’m planning on running outside in a t-shirt today).

There have been similar price increases throughout the energy complex--gasoline tends to grab the headlines, and has been somewhat spared--but the marginal increase in global demand in 2017 has been the big story, and the impact on headline inflation is likely to show up in early 2018 just as the Fed is wrestling with what to do next. At the very least, these price increases have to play a role in the December Summary Economic Projections...the dots.

The FOMC will have a tough time justifying headline inflation projections aren’t rising, and they have a preternatural desire to write off energy-driven inflation as a transitory factor. But time and again energy is the tipping point for changes in the speed of the economy. It will be acting as a brake here...leading to the flattening of the curve. That combination has painted the Fed into a corner. Do they have the guts to continuing hiking if the economy is doing well, headline inflation is pushing higher, but core continues to lag behind?

It seems like the answer is yes...can they get away with four hikes in 2018? If so, 2x10s is going to zero….

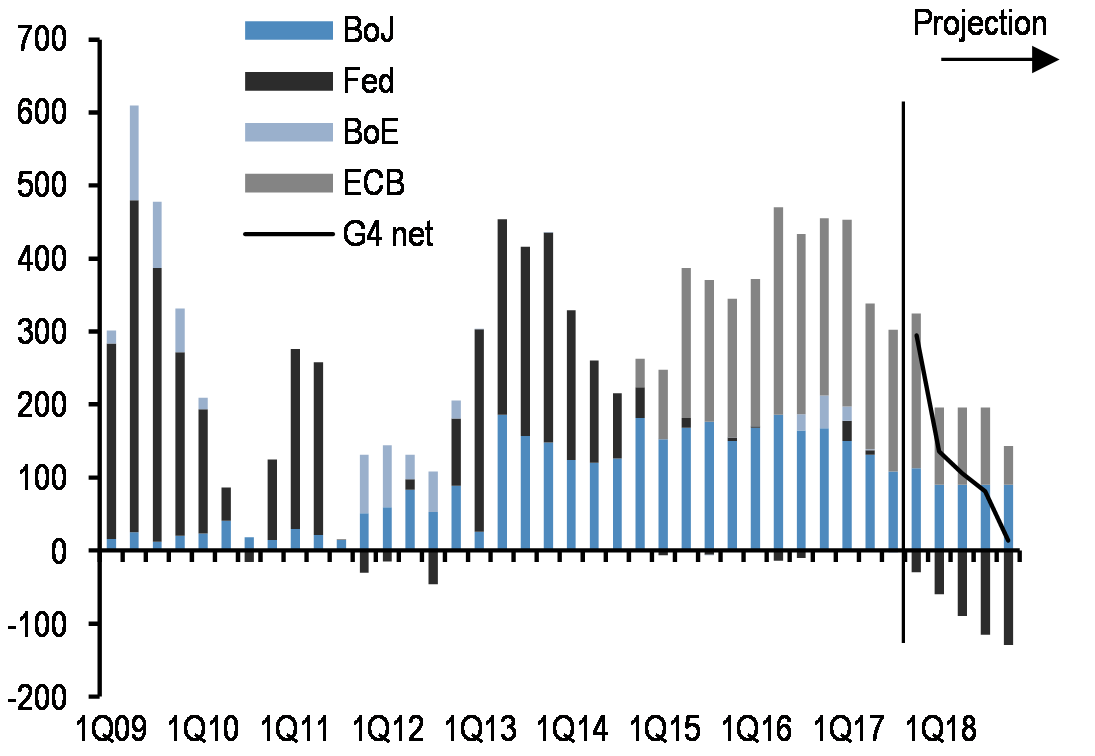

Absent a big move in core, what can change the demand for duration in the long end? Can this chart steepen the curve?

Or will US tax reform put a supply-side kick in the long-end? Supply doesn’t matter...until it matters. There will need to be a catalyst to change the narrative for buyers of duration...the demand side. I can’t see what it can be other than core inflation--probably on a global scale. While I continue to believe measures I have discussed in the past like the NY Fed’s underlying inflation gauge show there is price pressure in the economy, the market just won’t believe it until it really gets out of hand and forces the hand of not just the Fed, but of the ECB, BoJ, and even the PBoC.

Until then, the only thing out of hand is this flattening trend. And bitcoin.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

191 comments

Click here for comments